When it comes to municipal savings and reserves, there are two major players: Free Cash and Stabilization. The Massachusetts Division of Local Services (DLS) advises municipalities to create policies relating to such reserve funds to keep a cash cushion on hand in case of an emergency or financial crisis. Healthy reserve fund balances can make borrowing cheaper and easier for municipalities, as well.

Free Cash

Free Cash is money left over at the end of the fiscal year. The state must certify these funds before the town or city can use them as a revenue source for the next fiscal year’s budget. Certification takes place after June 30 and may not be completed until several months later, though the amount is considered “certified” as of July 1 of the current fiscal year. The Division of Local Services’ Technical Assistance Bureau suggests municipalities generate Free Cash at a rate of 3% to 5% of its yearly operating budget.

Free Cash is used exclusively for one-time expenses and to bolster stabilization accounts. The state frowns on using Free Cash to fund operating budgets.

Stabilization

Cities and towns can create several stabilization accounts, each with a particular purpose. Leverett has at least one Stabilization account; Shutesbury has both Stabilization and Capital Stabilization accounts. The DLS encourages the practice of generating multiple stabilization accounts, since it “stabilizes” a community’s finances, making an unexpected or emergency expense less apt to cause a fiscal crisis.

Free Cash: Leverett vs. Shutesbury

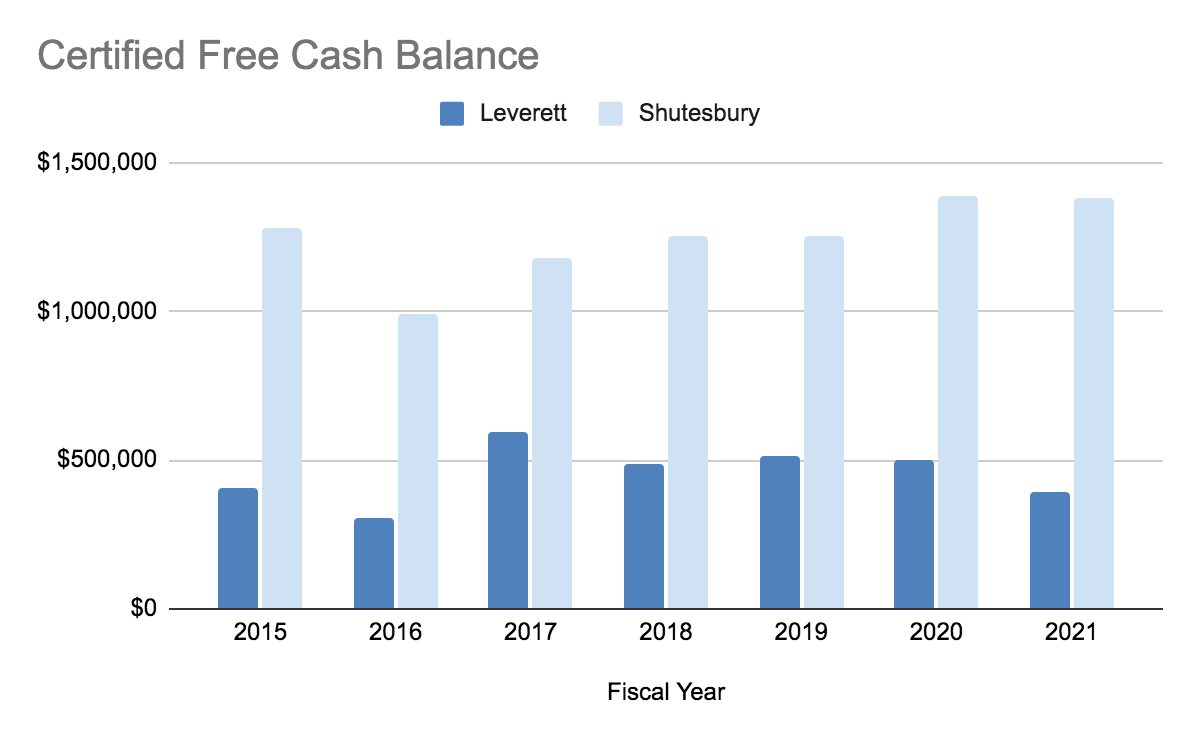

Since 2015, both Leverett and Shutesbury have maintained certified Free Cash levels of more than the suggested 3% to 5% of the town’s total annual budget. Where Leverett has had more of a struggle doing so, Shutesbury’s Free Cash is bursting at the seams.

From 2015 to 2021, Leverett’s Free Cash fund varied from a low of 4.90% in 2016 to a high of 9.18% in 2017.

During the same time period, Shutesbury’s percentage of certified Free Cash ranged from a low of 15.28% to an astonishing high of 21.53% of the town’s operating budget. For 2021, free cash was only slightly lower, at 19.73%.

What do Leverett’s and Shutesbury’s Free Cash levels look like in dollars? For last year, Leverett had $391,909 in its coffers, while Shutesbury’s fund totaled an impressive $1,378,767.

Why is there such a yawning chasm between the two towns’ Free Cash funds? It wasn’t a disparity between annual budget totals; both towns had budgets of approximately $6.9 million that year. And, despite the jaw-dropping difference in the two funds, Leverett was, at 5.60% of its budget, comfortably above the percentages suggested by the DLS.

It seems that Shutesbury just likes to save more than Leverett does. A lot more. Some might call it cash hoarding.

Shutesbury’s 19.73% represents a level of saving that seems exaggerated, particularly when you realize that taxpayers foot the bill for this account-padding. Fiscal year 2021 was also a pandemic year, which meant hardship for some residents. The Finance Committee acknowledged this by using $220,000 of Shutesbury’s Free Cash to lower the tax rate by $1.00.

For the current fiscal year, the tax rate rose to $23.37 from the previous year’s $22.61 even as the town declined to use Free Cash to pay for the Locks Pond Road culvert repair, electing to borrow the money instead.

Stabilization

When it comes to Stabilization, Leverett steadily increased its funding levels between 2016 and 2020, while Shutesbury maintained fairly high levels (between 14.29% and 15.63% of the annual budget) for the first three years before dropping off in 2019. Shutesbury’s appropriation was a mere 8.07% that year, and 10.17% in 2020. By contrast, Leverett’s 2020 appropriation was a robust 12.52%.

Overall, Shutesbury’s cash cushion is considerably larger than Leverett’s. Saving money for a rainy day is good fiscal policy, but too much of a good thing is expensive for taxpayers. Leverett is filling its coffers more slowly and maintains a much lower tax rate than Shutesbury--$20.39 compared to Shutesbury’s $23.37.

It appears we are paying dearly to have those reserves bulked up year after year. What motivates Shutesbury to sock away money to such an extravagant extent? There seems to be a story here, which I’ll examine next time.