On the evening of August 17, I attended the Small Library Pilot Project informational meeting hosted by Lauren Stara and Andrea Bunker of the Massachusetts Board of Library Commissioners under the pavilion at the Shutesbury Athletic Club. Along with approximately 100 other town residents, I listened to these two women, both Library Building Specialists, as they discussed various aspects of the Pilot Program.

The meeting was certainly informative but it was something else, too. I got the impression it was more of an enthusiasm-building endeavor for a structure that would not fit most people’s definition of a “small library”--in either footprint or cost.

Here are my three main takeaways from the meeting, each of them a complete surprise to me.

As Ms. Stara described the genesis of the Small Library Pilot Project, it became apparent how involved she has become with the concept.

She noted that other construction grants were difficult for smaller towns to navigate and that what the state has been doing in the past needs to change. She specifically mentioned the 15-year waiting list, saying that is not workable. She also noted the “blood, sweat, and tears” that went into creating the new guidebook, Library Space: A Planning Resource for Librarians, on which she worked for over a year and envisions being used as a model for new library construction across the state of Massachusetts and, perhaps, nationally.

As she began taking questions from the audience about the pilot program, she noted that the most common regret she heard from library officials with completed projects was that they should have gone “bigger”.

As for square footage, Ms. Stara said that would depend upon input from the Library Director and “whoever wants to participate”. This input would be things like the type of “spaces and services (Shutesbury) need(s)” as well as the size of these spaces based on “projected attendance”. A very vague and subjective process, to be sure.

Later, audience members were encouraged to shout out the types of rooms, spaces, and services they “dream” about. Cries of “a real bathroom” and “running water” were augmented by suggestions for a cafeteria, project rooms, soundproof rooms, teen space, exercise space, meeting and cross-generational space, a “beautiful space to meet your friends and neighbors and have a conversation” as well as “adequate staffing space”--to which Ms. Stara replied, “We’ll get Mary Anne an office.”

On August 30, a small group of Shutesbury residents and the MBLC Representatives toured the new library in Erving, a town of similar population size but with a 2021 residential tax rate of $7.59 compared to Shutesbury’s $22.61. Erving’s library is 8,200 square feet. Ten years ago, Shutesbury was proposing a library of 5,800 square feet. Where will we end up this time? If dreams win out over need, we may be asked to fund a bigger library than most residents ever imagined.

“Community Need” is an Amorphous Concept

The idea of “community need” is an important part of the pilot project and is mentioned twice in the list of six criteria for Boston’s review and ranking of applicants for the program. During the presentation, this concept was given short shrift when Ms. Stara mentioned only the use of state income per capita and equalized values (total value of property in the town).

Thinking there must be more to the issue than just income and values, I emailed Ms. Stara and asked what other criteria the Board might consider, such as lack of home-based broadband or reasonable access to a larger library. She replied that both of those concerns were valid and towns were encouraged to state their own specific needs in their Letters of Intent. She also mentioned that statements of need can be adjusted when the formal application is submitted in November.

Therefore, there are two distinct concepts of need:

➤Financial/economic need, as reflected in state data on income and property values;

➤Perceived need, as stated by the library officials who fill out and submit the paperwork required to participate in the contest called the Small Library Pilot Project.

The first category is very data-driven, with no room for debate or discussion.

The second category, however, is entirely subjective and based mostly upon the concerns, wants, and needs of those whose job is to promote and encourage enthusiasm about libraries.

The MBLC will eventually make a decision based, at least partially, on these subjective needs. Now that the competition is between only Shutesbury and Otis, the wording of this criterion could be crucial.

Currently, Shutesbury library officials are soliciting input from residents regarding what they desire in a new library (more on this later). No doubt these “wish lists” will be included in the application due in November.

Shutesbury Voters Must Commit Money to this Project Before the Scope and Costs are Known

This is HUGE!

Although this subject was raised at a meeting on August 3 between MBLC’s Stara and Bunker and various Shutesbury town officials, the sound quality was so poor at that hybrid meeting that I missed it.

This aspect differs from the state’s other library construction grant programs and Ms. Stara admitted that this will be a difficult concept for small towns. It is a firm requirement, however, and she noted that the town meeting vote for a monetary commitment will be based on cost estimations, not actual costs. The grant will pay 75% of actual eligible costs if the project price tag rises above the estimate as construction gets underway. Because not all costs are “eligible”, the grant is guaranteed to pay less than 75% of the total project cost.

Ms Stara did not clarify whether the grant funds would be disbursed before or after construction. Without upfront funding, Shutesbury might have to foot the bill, at least temporarily, until funding comes through. If so, this could be a significant strain on our town’s finances.

Ms. Stara also noted that, although construction costs have receded from their recent highs, those costs always move in an upward trajectory; that is something we need to keep in mind.

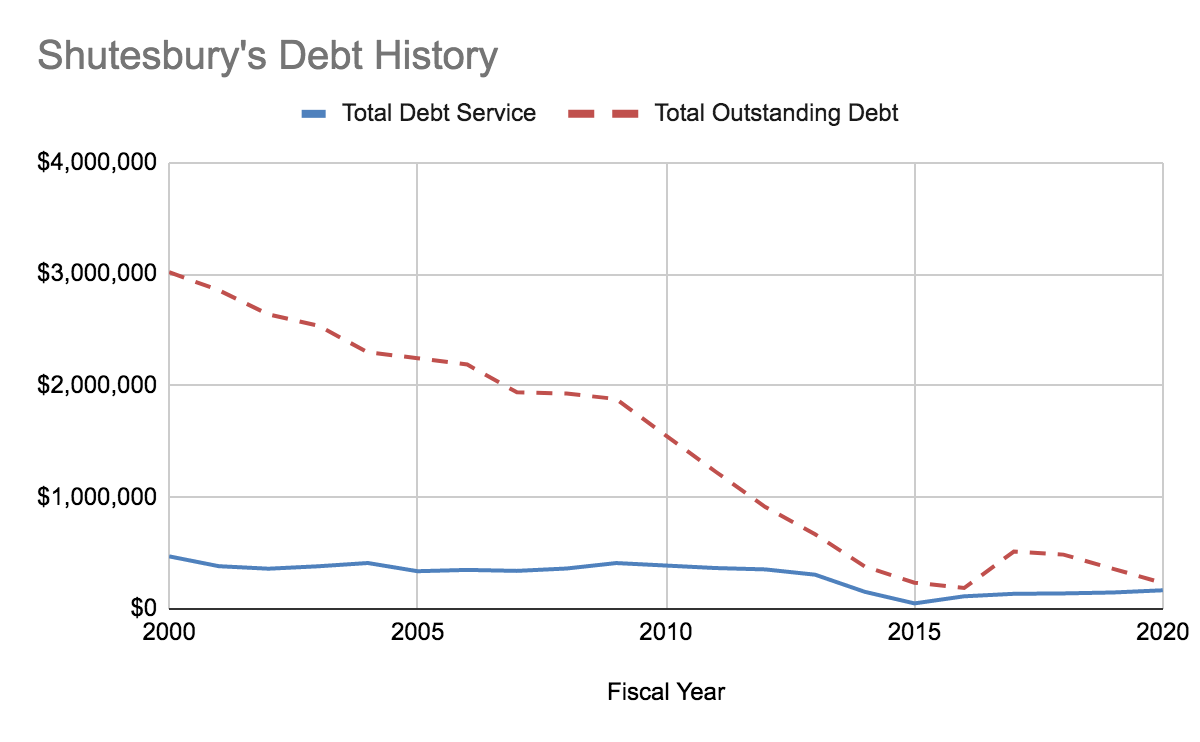

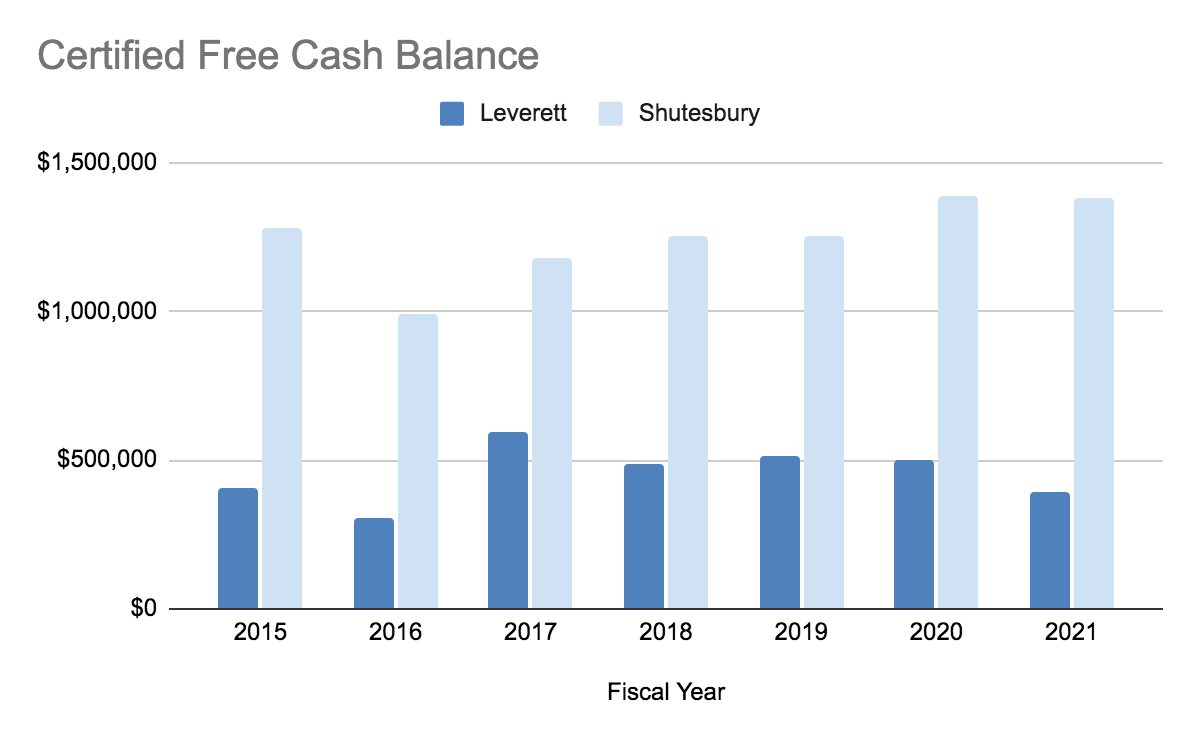

Since construction would not begin until 2023 (if Shutesbury is chosen), costs could be a lot higher than they are today. We have recently learned that inflation and supply-chain disruptions can occur during a crisis and linger for months (or years). Do we want to risk our nearly debt-free and high-savings status on just one project?

It’s worth thinking about.